Kuroto Fund, L.P. - Q4 2023 Letter

Dear Partners and Friends,

PERFORMANCE

Kuroto Fund, L.P. rose 1.07% in the fourth quarter and 19.46% for the full year.

By comparison, the EM index gained 5.6% in the fourth quarter and 10.3% for the full year 2023.

A breakdown of Kuroto Fund's exposures and contribution can be found here.

By way of update on the loss sustained in January of 2023 as a result of a post-execution error involving one of our service providers and FX trades in Nigerian Naira. With assistance from our outside counsel, through arbitration, we were able to recoup a portion of the loss. We have closed this matter and received all loss mitigation proceeds into the Kuroto Fund, LP account.

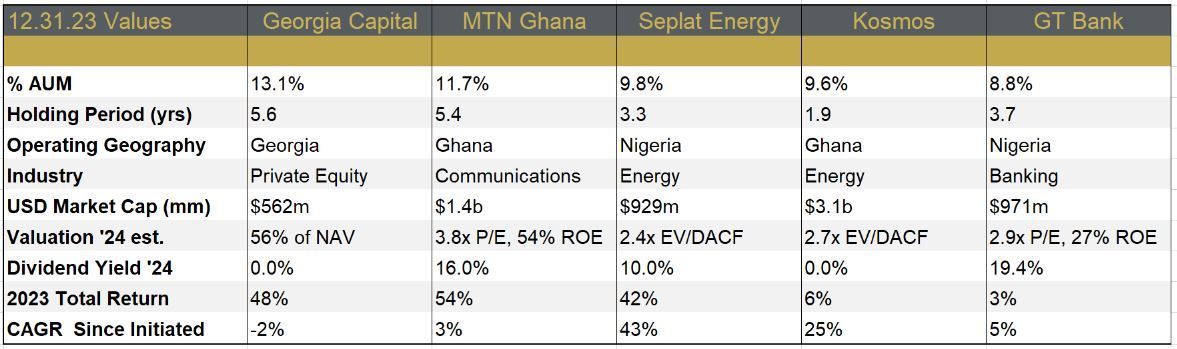

investment Thesis Review for top 5 Positions by Portfolio Weight

Georgia Capital

Georgia Capital is a London listed holding company with investments in the Republic of Georgia. The group owns 20% of the Georgia’s most profitable bank, largest hospital chain, largest pharmaceutical chain, largest private education group, largest insurance business, a Heineken brewery group, and a vineyard. Georgia Capital trades at roughly half of our estimate of NAV and approximately 4x look-through earnings.

In 2023, Georgia enjoyed a third consecutive year in a row of strong economic growth. After growing 10% in real terms in ’21 and ’22, the country’s economy grew by 6.8% in 2023. The country’s debt to GDP ratio, which peaked at just over 60% during the pandemic, has come down to less than 40% and inflation is again below 2%. This backdrop has provided a tailwind for Georgia Capital’s businesses, especially the bank, which continues to generate close to a 30% ROE on conservative capital ratios. The bank grew its book value 20% in the year while paying out ~10% of its market cap in dividends and share buybacks.

Georgia Capital took advantage of its record cash flow generation to refinance their 2024 debt. After repaying $100 million USD of the debt early, the group refinanced $200 million for 5 years at 8.5% fixed. This refinancing leaves Georgia Capital with a conservative leverage position at less than 15% of group NAV, a position that allows ongoing cash flow to be used in share buybacks, the most attractive capital allocation decision given the stock’s large discount to NAV.

Going forward, we expect the group’s businesses to continue to grow. In 2024, the bank should generate double digit growth while paying a large divided. We expect the other core businesses – healthcare, education, and insurance – to grow earnings by over 10% this year. We also expect the group to trim its investments in capital-intensive businesses, specifically the brewery, wine, real estate, and renewable energy business lines.

MTN Ghana

MTN Ghana, the largest telecom and mobile payments provider in Ghana, generated a 54% return on equity and delivered a 16% dividend yield last year. The company trades at just 3.7 times our estimate of 2024 earnings. Owning such a high-quality business at such a low valuation is attractive even if the Ghanian macroeconomic backdrop remains rough.

Through the first nine months of 2023, MTN Ghana grew revenue and earnings over 30%. This growth outpaced the 24% devaluation in the Ghanian Cedi last year. Inflation in Ghana has begun to normalize, dropping from a peak of 50% to 26% at last count. On the back of the country’s sovereign default, Ghana adopted an IMF program. This program should help the country make some of the necessary, and long overdue reforms. Even so, the Ghanian macroeconomic backdrop remains challenging.

If Ghana’s macro environment does begin to improve, MTN Ghana is well positioned to add to its 2023 growth rate. Additionally, the local stock market should see renewed interest in 2024 as the yield on Ghanian government debt falls. In a slightly more normal macroeconomic environment, we believe that MTN Ghana should trade at twice its current multiple. Even in a difficult economic environment, we expect MTN to maintain margins while paying out most of the earnings as a dividend.

Seplat Energy

Seplat Energy is an oil and gas company with onshore and shallow offshore fields in Nigeria. The company produces around 50k barrel of oil equivalent per day and offered a 10% dividend yield as of year-end 2023. Seplat is exposed to two potentially transformative events, a large-scale onshore gas project and an offshore oil acquisition. The successful completion of the project or the transaction would make Seplat one of Africa’s largest energy companies.

The potentially transformative gas project is the Anoh Gas Processing Plant. This project will make Seplat one of Nigeria’s largest suppliers of natural gas to the Nigerian power grid. A partnership between Shell, Nigeria’s national oil company and Seplat, the Anoh gas project is expected to come online later this year. Once complete, Seplat’s group production will rise from 50k boepd to over 70k. While the project is already a few years behind schedule, we believe that the project should finally be completed this year.

The potentially transformative offshore oil acquisition is Seplat’s acquisition of Exxon Mobil’s shallow water asset in Nigeria. In 2022, Seplat announced an agreement with Exxon to purchase 100k barrels of oil per day shallow water production. The production comes with one of the Nigeria’s largest oil export terminals and enough natural gas reserves for a greenfield LNG project. The agreed-upon price is attractive enough to encourage an assortment of well-connected Nigerians to attempt to purchase the assets in lieu of Seplat. Exxon Mobil, however, has no desire to sell to an entity with questionable corporate governance that lacks the necessary operational expertise. Accordingly, Exxon Mobil has been clear that they wish to sell only to Seplat.

Nigeria’s newly elected president – keen to increase investment into the oil sector – understands that the Exxon Mobil - Seplat transaction is a prerequisite to meaningful additional investment in the sector. Based on our meeting with several interested parties in Lagos this past November, we believe the deal is likely to proceed. If both the Exxon Mobil acquisition is consummated and the Anoh gas project is completed this year, as we think is likely, Seplat’s annual cash flow will rise to well over one billion dollars, which is more than the company’s current market cap.

Kosmos Energy Ltd.

Kosmos Energy is an offshore oil and gas company with assets in the Gulf of Mexico and off the west coast of Africa. The company is in the final stages of a multi-year growth plan that will take production from ~60k to ~90k boepd by mid-2024. At $70 Brent and ~90k boepd, Kosmos will generate ~$500 million USD per year in free cash, a 16% free cash flow yield. At an $80 Brent oil price, the free cash likely grows to $750mn, or a 24% free cash flow yield.

The centerpiece of the company’s growth plan is the Tortue field located off the coast of Mauritania and Senegal. This multi-billion-dollar development is a 50/50 partnership with the supermajor BP. The Tortue field, which is estimated to hold more than 15 trillion cubic feet of gas, will begin producing ~2.5 million tons of natural gas this year with an estimated 30 years of reserve life. Importantly, the Tortue field is just one part of the significant acreage Kosmos holds in Mauritania and Senegal where their total estimated inventory ranges from 50-100 tcf of gas. Kosmos plans to bring additional LNG projects online from these fields every couple of years over the next decade.

The development of such a massive LNG project requires a world-class team. BP is the operator, but Kosmos discovered the assets and is working closely on all aspects of the project. Kosmos’ close partnership with BP is a testament to the quality of the team that Kosmos’ CEO, Andy Inglis, has built. Andy, the former head of BP’s global exploration and production business, has been able to attract top tier talent as the supermajors de-emphasized deep water exploration.

Andy also understands the importance of generating a rapid payback on Kosmos’ investments. Accordingly, he has organized the Kosmos portfolio around existing infrastructure, allowing for quick and cheap tiebacks in the case of exploration success. Once Kosmos’ first LNG project is online next year, we expect Kosmos to re-rate significantly. Longer term, we expect Kosmos to continue to grow by bringing their already discovered resources online with internally generated capital.

Guaranty Trust Holding Company

Guaranty Trust is Nigeria’s best bank. Known for the honesty of its management, the trustworthiness of its financial statements, conservative lending practices, and a low cost structure and higher profitably, Guaranty Trust is unique among Nigeria’s banks. Guaranty Trust generates a sector-leading ROE of about 30% and at year-end, traded at 2.9x our forecast of ’24 earnings, 0.8x book, and offered a 19% dividend yield.

Nigeria’s economic and political backdrop is improving. The new government devalued the currency, ended the fuel subsidy, and is focused on boosting the country’s oil and gas production. Guaranty Trust was well positioned for this devaluation with its large USD asset mix and short duration investment book. In the first 9 months of 2023, Guaranty Trust booked a gain of 384bn Naira from the devaluation, equivalent to 34% of the group’s market cap. Further gains are likely to come as the Nigerian currency falls further. In addition to these gains, the higher interest rates are helping Guaranty Trust boost its net interest income which will allow for sustained higher profitability going forward.

When the Nigerian economy eventually normalizes, Guaranty Trust will be in a perfect position to capitalize on a return to strong growth. Given Nigeria’s low financial products penetration rate, there is white space to grow the loan book. Moreover, many of Guaranty’s peers are short of capital due to the difficult economic environment. Guaranty does not have the same issue and will be positioned to grow its loan book rapidly when the environment improves whereas its peers will be forced to retain capital to increase reserves.

organizational Update

In December, we parted ways with Daniel Schreck and Stephen Saroki.

Daniel joined Equinox Partners in 2009. Over the past 14 years he worked closely with our clients, cultivated new prospects, and oversaw a significant upgrade in our client communications. Daniel’s client responsibilities have been assumed by Kieran Brennan, who joined us in January 2021 and has been working with Daniel for the past 3 years.

Following a summer internship in 2016, Stephen Saroki joined our team as a full time research analyst in 2018. While a generalist by training, Stephen spent most of his time analyzing gold and silver miners. His company coverage has been picked up Coille, Alfredo, and Sean.

We wish both Daniel and Stephen well in their next endeavors. Our team of 11 professionals now consists of six investment professionals and five in operations.

Sincerely,

Sean Fieler Brad Virbitsky

[1] Please note that estimated performance has yet to be audited and is subject to revision. Performance figures constitute confidential information and must not be disclosed to third parties. An investor’s performance may differ based on timing of contributions, withdrawals and participation in new issues.

Unless otherwise noted, all company-specific data derived from internal analysis, company presentations, Bloomberg, FactSet or independent sources. Values as of 12.31.23, unless otherwise noted.

This document is not an offer to sell or the solicitation of an offer to buy interests in any product and is being provided for informational purposes only and should not be relied upon as legal, tax or investment advice. An offering of interests will be made only by means of a confidential private offering memorandum and only to qualified investors in jurisdictions where permitted by law.

An investment is speculative and involves a high degree of risk. There is no secondary market for the investor’s interests and none is expected to develop and there may be restrictions on transferring interests. The Investment Advisor has total trading authority. Performance results are net of fees and expenses and reflect the reinvestment of dividends, interest and other earnings.

Prior performance is not necessarily indicative of future results. Any investment in a fund involves the risk of loss. Performance can be volatile and an investor could lose all or a substantial portion of his or her investment.

The information presented herein is current only as of the particular dates specified for such information, and is subject to change in future periods without notice.