Kuroto Fund, L.P. - Q4 2021 Letter

Dear Partners and Friends,

PERFORMANCE & PORTFOLIO

Kuroto Fund declined -3.7% in the fourth quarter of 2021 and was up +22.1% for the full year. By comparison, the EM index declined -1.3% in the fourth quarter of 2021 and -2.2% for the full year. [1]

Our 2021 gains were primarily driven by FPT and MTN Ghana, with 18 companies overall delivering positive contributions. Five of our companies posted a loss during the year, Guaranty Trust and our Turkish investments most notably. At 5.6x earnings, 23% earnings growth, 19% ROEs, and a 6.4% dividend yield in 2022, our portfolio continues to combine value and quality.

yearend Top-five holdings

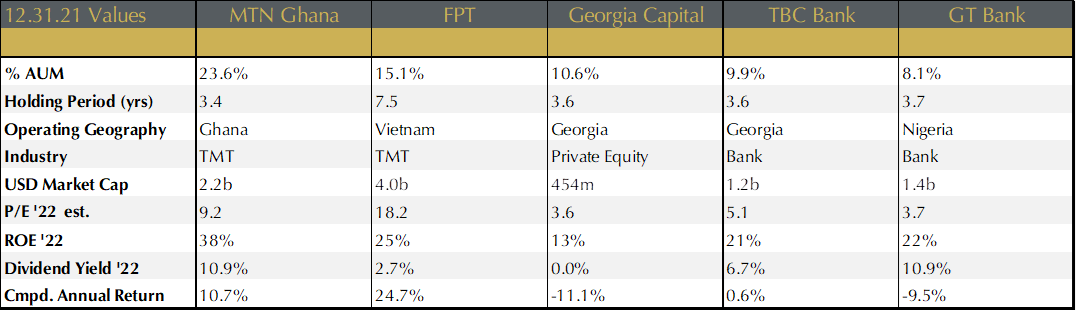

Our five largest investments going into 2022 are MTN Ghana, FPT, Georgia Capital, TBC Bank, and Guaranty Trust. While that remains largely unchanged year over year, Logo Yazilim was replaced by Georgia Capital as its shares declined and Georgia Capital's gained in 2021. Logo remains our sixth largest position.

MTN Ghana

MTN Ghana, the country’s dominant telecom and mobile-money platform, had a strong year operationally and a tough year politically. Through September, revenues grew close to 25% year over year and earnings grew 34%. This strong growth was driven by data and mobile-money revenue, both of which likely grew over 40% for 2021. Unfortunately, MTN’s success attracted the attention of the Ghanian government which is desperate for tax revenue. The government’s proposed 1.75% transaction tax on mobile money transactions will, if passed, impair MTN’s mobile-money business which accounts for 20% of its revenues.

MTN Ghana drew the government’s scrutiny because of its dominance. The company’s high revenue market share generates an even higher profit share. This allows MTN to re-invest into its network at significantly higher rates than its competition which in turn reinforces its competitive advantages. The company’s mobile-money business, MOMO, is particularly strong. MOMO has an estimated market share north of 80% despite competitors offering the service for free. MTN is able to maintain this position due to the large network effect that emerges from the company’s large installed base, large agent network, and deep integration into merchants. Over half of the country’s adult population are active users of the service and its agent network and integrated merchants both number over 200k.

We expect strong growth in MTN’s telecom business to continue while the fate of MTN’s mobile money business depends on the transaction tax. If implemented, the 1.75% transaction tax would drive a precipitous decline in mobile-money usage. Several years ago in Uganda a similar tax was implemented and usage dropped 38% before it was repealed. That said, mobile-money is much more integrated into Ghanaian society today than it was in Uganda at the time.

Assuming the 1.75% transaction tax is implemented and MTN’s mobile-money service falls by half, we estimate that the company’s overall revenues would be flat for a year and earning would decline 10%. In this scenario, the stock would trade around 9x earnings in ’22, 7x in ’23, and would still generate a 38% ROE. If the tax does not pass, MTN is trading at closer to 6x earnings with a mid-to-high teens dividend yield. In sum, MTN remains an attractive investment but is obviously less attractive if the 1.75% transaction tax passes.

FPT

The dominant Vietnamese tech company, FPT went from strength to strength in 2021. The company’s revenue and profits grew ~20% for the year. This growth was in large part driven by FPT’s global IT services business. The high value-add digital transformation portion of its global IT services business grew 76% for the year and now makes up almost 40% of its global IT revenue.

IT spending continues to increase globally and Vietnam’s position as a global, low-cost leader continues to improve as wage inflation in India and China remain faster than wage inflation in Vietnam. This wage inflation advantage, combined with FPT’s efforts to move up the value chain, should provide a tailwind to growth in 2022. In addition to its export business, FPT is making sizable investments into cloud-hosted software and services for Vietnam’s small and medium-sized enterprises.

FPT’s financial results have been consistently strong. The company has no debt, generates a 20% ROE, and has had little trouble maintaining margins. Over time as FPT’s software business grows, we believe the company’s financial characteristics will improve. Margins and cash generation should both grow faster than the top line. Despite all these strengths, FPT is trading at 17x 2022 earnings. The company has a long runway of growth ahead of it and remains a sizeable holding in the fund.

Georgia Capital

By selling its water-utility business in 2021, Georgia Capital proved that it can monetize its investments and took a huge step to close its holding company discount. Georgia Capital trades at roughly 50% of the SOTP, and the water business sale will generate almost half of the market cap in cash.

Each of Georgia Capital’s core businesses performed well in 2021. The bank is on pace to generate a 20%+ ROE for the year, grow loans double digits, and to pay a dividend. The healthcare business, which controls roughly 40% of the country’s hospital system, recovered in 2021 after the pandemic caused many elective visits to be deferred. Revenue was up 49% in the first 9 months of the year and EBITDA was up 78%. The healthcare business has completed its capital buildout and is contributing dividends to the holding company. The pharmacy business—a beneficiary of the pandemic—continued to grow in 2021, with EBITDA up 7% in the first 9 months of the year. Finally, the water-utility business saw a strong recovery from last year when a drought limited its ability to sell excess electricity. Most importantly, Georgia Capital sold the water utility business to a strategic buyer on the last day of 2021.

FCC Aqualia, a Spanish water company, agreed to pay $180m for 80% of Georgia Capital’s water utility. This $225 valuation represents a 30% premium to the $173m valuation applied by Georgia Capital. This sale is beneficial to the holding company for three reasons. First, it proves the merits of its overall PE-like investment model. Georgia Capital made 2.7x its money in USD terms and generated a 20% USD IRR on its investment in the business. Second, it shows that there is interest from outside parties in its Georgian assets at valuations near or above the company’s internal valuations. Finally, it gives the company liquidity to buy back shares at what remains a large discount to the sum of the parts.

TBC Bank

TBC maintained its market position, returned to peak profitability, and reinstated its dividend. In addition to its participation in Georgia’s profitable banking duopoly, TBC doubled down on its investment into Uzbekistan. In our opinion, TBC’s stock remains meaningfully undervalued at 0.8x book value, 4.4x earnings, and an 8% dividend yield for 2022.

TBC and Bank of Georgia control over 70% of the market for banking services in Georgia. Both banks earn over 20% ROEs and grow loans double-digits. TBC took a large provision in 2020 at the start of the pandemic in an attempt to frontload the impact of the crisis. As it turns out, the provisions were overly conservative and the bank was able to earn extraordinary profits in 2021 as a result of this over-provisioning. Going forward, TBC expects provisioning to normalize around 1% and its ROE to remain over 20%. In the second half of 2021, as it became clear the pandemic-related provisioning was sufficient, the bank reinstated its dividend.

TBC’s entry into Uzbekistan is going better than expected. The opportunity is large with a sizeable underbanked population in a nation that is over 8x the population of Georgia. TBC has two businesses in the country, one is a leading mobile-money transfer business and the other is a digital bank. The money transfer business already has one million active customers and is growing revenue/transactions over 50% per year. The digital bank is the bigger opportunity in Uzbekistan, and they have an offering that is unmatched in the country. Despite having just launched the digital bank this year, it already has over one million downloads.

Guaranty Trust

Guaranty Trust is a solvent, trustworthy, professional financial institution in Nigeria. As a result of this unique position, Guaranty Trust is able to generate excellent returns while taking very little credit risk. The bank has consistently achieved 20%+ ROE.

In 2021, Guaranty Trust successfully converted into a holding company and separated its bank from its digital payments business, wealth management, and insurance businesses. Guaranty Trust’s digital payments business is doing particularly well, having grown revenue 91% YOY in Q3 '21.

Despite having much potential, Nigeria continues to disappoint investors. The Nigerian Central Bank’s policy of holding the country’s currency at an artificially high rate vs. the USD and keeping interest rates far below inflation has scared off all but the most intrepid of foreign investors. Local conflicts have further damaged the country’s attractiveness as an investment destination by taking oil production offline and limiting the country’s ability to generate foreign exchange revenues.

The situation in Nigeria should improve some in 2022. After years of delay, a massive refinery is expected to come online late this year. Once at full capacity, it should alleviate the country’s need to import refined fuel. Further new investment into the country’s oil sector should help the country’s domestic oil production and its foreign exchange reserves to recover. On the other hand, the current administration’s unfortunate set of macroeconomic policies are likely to persist until the elections of 2023.

GT Trust trades at 0.7x book and 3.6x earnings while paying an 11% dividend yield. Even if Nigeria remains a political mess, GT Trust is positioned to generate excellent returns for years to come in our opinion.

Sincerely,

Sean Fieler Brad Virbitsky

END NOTES

[1] Performance stated for Kuroto Fund, L.P. Class A on a net basis. An investor’s performance may differ based on timing of contributions, withdrawals, share class, and participation in new issues. Unless otherwise noted, all company-specific data is derived from internal analysis, company presentations, or Bloomberg. Company valuations and exposures are as of 12.31.21.

Endnote: Unless otherwise noted, all company-specific data derived from internal analysis, company presentations, Bloomberg, or independent sources. Values as of 12.31.21, unless otherwise noted.

This document is not an offer to sell or the solicitation of an offer to buy interests in any product and is being provided for informational purposes only and should not be relied upon as legal, tax or investment advice. An offering of interests will be made only by means of a confidential private offering memorandum and only to qualified investors in jurisdictions where permitted by law.

An investment is speculative and involves a high degree of risk. There is no secondary market for the investor’s interests and none is expected to develop and there may be restrictions on transferring interests. The Investment Advisor has total trading authority. Performance results are net of fees and expenses and reflect the reinvestment of dividends, interest and other earnings.

Prior performance is not necessarily indicative of future results. Any investment in a fund involves the risk of loss. Performance can be volatile and an investor could lose all or a substantial portion of his or her investment.

The information presented herein is current only as of the particular dates specified for such information, and is subject to change in future periods without notic