Equinox Partners Precious Metals, L.P. - Q1 2021 Letter

Dear Partners and Friends,

PERFORMANCE & PORTFOLIO

Equinox Partners Precious Metals Fund, L.P. declined -14.6% in the first quarter of 2021. By comparison the GDXJ index declined -17.0%, the HUI index fell -11.1%, and gold and silver declined -9.8% and -7.4% respectively. For the year to date through April 30th, we estimate the fund was down -5.9%, while the HUI declined -7.7%, the GDXJ fell -12.5%, gold declined -7.1%, and silver fell -2.5%.

Inflation and gold

In the first quarter, inflation was up, concern about inflation was way up, and gold mining stocks were way down. At its March 30th intraday low, the GDXJ junior gold mining index was down 20% for the year to date after having endured a cumulative $265m outflow. What gives? Rising inflation has historically been good for gold and negative for non-resource stocks and bonds.

Bond investors possess the type of complacency that can only be induced by an almost forty-year long bull market. The U.S. 10-year Treasury is not just yielding less than inflation but also less than the Fed’s inflation target. Investing in bonds has been described as “senseless” by Paul Singer and “stupid” by Ray Dalio. Fixed income investors’ concern about inflation eating into their real return is offset by their confidence that central bankers will protect them from losses. The consensus seems to be that even if the inflation picture deteriorates, fixed income owners will be given time to allocate their largely intact capital elsewhere. This reasoning does not, however, make bonds good investments; it only makes them less prone to collapse than equities.

Equity investors, by contrast, are acutely aware of the rapidity with which stocks can decline. They are simply not convinced that the coming inflation is going to be bad for stock prices. Many money managers are nonchalantly insisting that stocks are the best hedge against inflation. Part of this optimism stems from a healthy dose of recency bias. The last several inflationary episodes in the developed world have been associated with strong growth and a rising stock market. The 2005-2008 high-growth inflation uptick is a case in point. Over those three years, as the world went through a synchronized expansion, U.S. inflation averaged 3.3% and the S&P rose over 30% before the ’08 selloff.

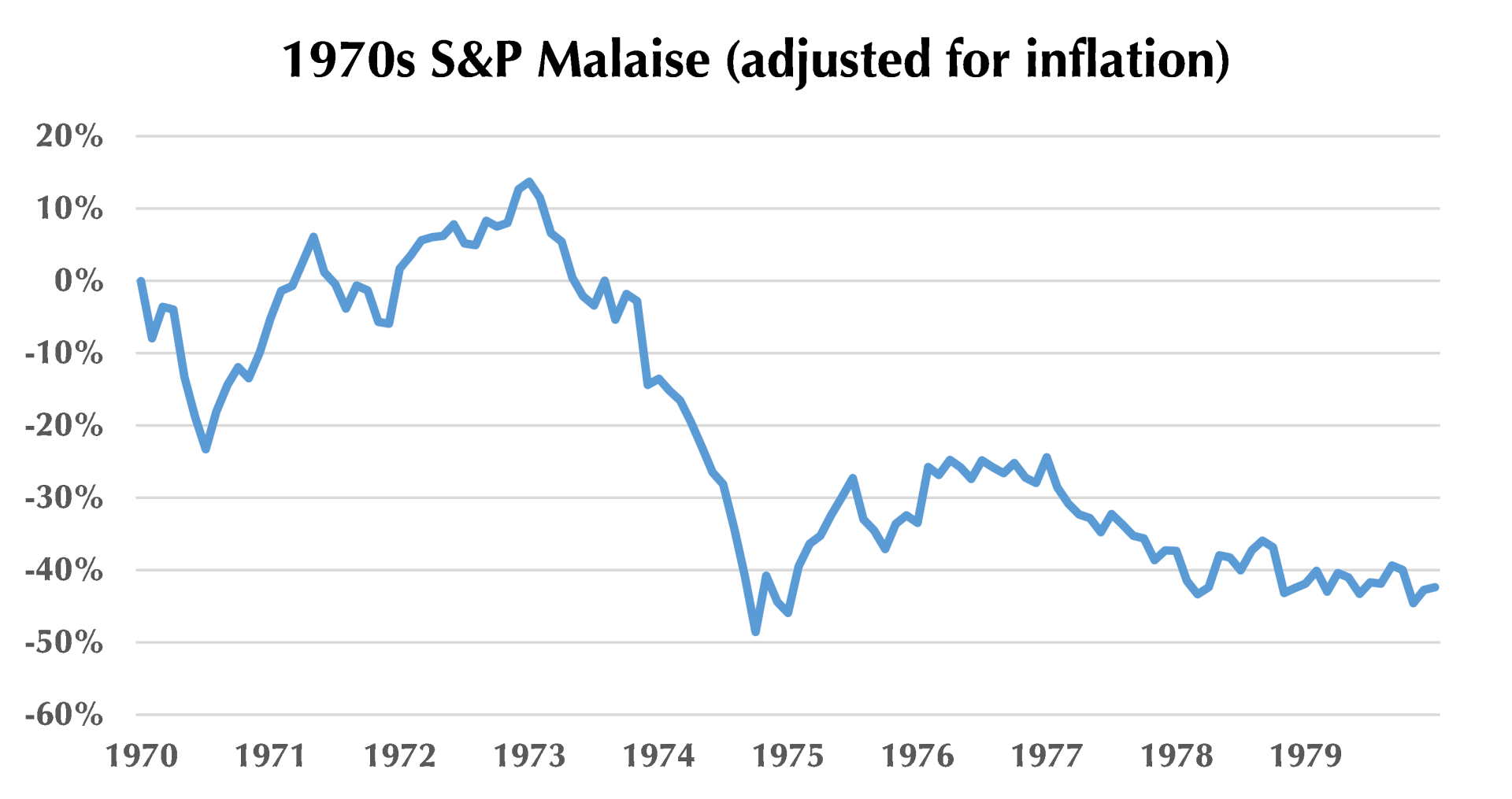

While the 2005-2008 period proves that inflation need not be bearish for equities, it is equally true that the 1970s inflationary experience was catastrophic for equities. It is worth recalling the horrible details. From January 1970 to January 1980, the S&P lost 42% of its value in real terms. It took the S&P 14 years to permanently break through its late ‘68 peak in nominal terms. Even with dividends reinvested, in real terms the market did not exceed its 1968 peak until 1983, 15 years later!

There are, of course, many differences between today and the 1970s. Most importantly, the 1970s lacked the trifecta of globalization, demography, and technology that has suppressed inflation for a generation. Central bankers believe that these forces are so deflationary that even if they can engineer 2% inflation it will be difficult to sustain. As such, central bankers reason that while consumers may face a loss in purchasing power associated with a bout of inflation, they should not get all worked up about the long-term consequences.

We also appreciate the extent to which globalization, demography, and technology have made it hard to generate much inflation. It’s not, however, at all clear to us that when higher inflation does arrive it will be either benign or transitory. In our estimation, the crazy combination of fiscal and monetary policy necessary to achieve policymakers’ desired inflation rate will be very hard to walk back. The Fed and Congress are addicted to massive money printing and spending, respectively. We doubt either institution possesses the chops to change course when the time comes, and that question looks increasingly relevant given the recent data. Nominal GDP grew 10.7% in Q1, CPI ticked above 2.5%, personal incomes were up 21% month over month in March, this year’s budget deficit is running in excess of $2 trillion, and the Fed is still growing its balance sheet at $120 billion dollars per month[1].

With an inflationary wave fast approaching, it is clear to everyone that government policy is the underlying cause. Government culpability is critical, not because we are interested in assigning blame, but because government-led inflation mirrors the 1970s rather than the more benign bouts of growth-driven inflation since then. From the failure of the Russian wheat crop in 1972 to the chip shortages of 2021, inflation typically begins as a series of idiosyncratic events. Overconfident central banker invariable rationalize inaction at these critical moments. Herb Stein’s case for easy money in 1971 eerily echoes the Fed’s arguments today: “We’re a long way from full employment, we still have a lot of room for expanding the economy, and the inflation rate is low.” Herb Stein later added, “We misinterpreted.”[2]

The Fed is, of course, not solely to blame for the building inflationary forces. Just as in the early 1970s, the underlying cause of inflation is government policy writ large. For over a year, both the expansions and contractions in the U.S. economy have been dictated by government action. Government mandated lockdowns of the entire service sector are clearly more disruptive than the wage-price controls of the early ‘70s. The stimulus checks are larger than any direct benefit the government has ever provided. As a result, we have an economy expanding and contracting because of government policy rather than market forces.

Having assumed responsibility for the business cycle, the federal government will find it difficult to withdrawal its support. There is never a politically expedient time for a recession. Neither political party is going to subject the American electorate to a fiscal cliff prior to the 2022 mid-terms. The same will hold true for 2024. Monetary policy promises to remain equally feckless and accommodative. At some point, the Fed will have to choose between persistent inflation or taking a step back as markets find a lower level. Both scenarios will be made worse by a Fed Chairman who appears weak and unable to make tough choices.

[1]

BEA

[2] Wyatt C. Wells. Economist in an Uncertain World: Arthur F. Burns and the Federal Reserve, 1970-1978. Columbia University Press, 1994

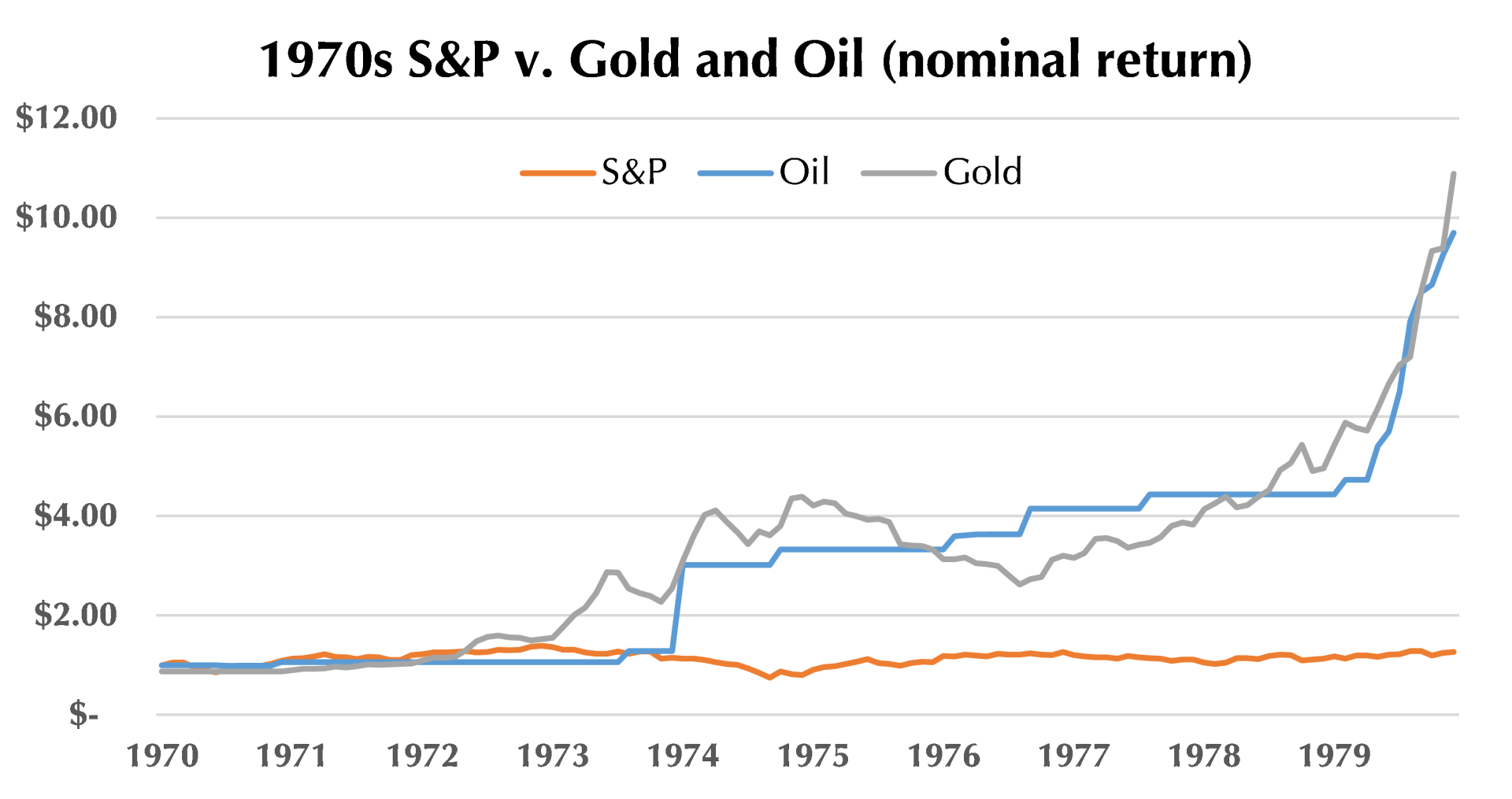

As the graph makes clear, government-induced inflation has historically been good for precious metals and energy and disastrous for non-resource common stocks and bonds. We expect our portfolio to outperform as the government-led inflation cycle builds. Long-term investors who sense the status quo is changing should aggressively reduce their exposure to fixed income and growth stocks and reallocate their capital to commodities, generally, and precious metals equities, specifically.

Organization

In January, we welcomed Kieran Brennan to our investor relations team. A Williams grad, Kieran previously worked at First Eagle, Connor, Clark, & Lunn, and the MFA.

Sincerely,

Equinox Partners

[1] Sector exposures shown as a percentage of 03.31.21 pre-redemption AUM. Performance derived from Equinox Partners Precious Metals Fund, L.P. and is not indicative of an investment into the offshore fund nor gold and silver mining managed accounts managed by Equinox Partners Investment Management, LLC. Performance will differ based on the account and timing. Unless otherwise noted, all company data is derived from internal analysis, company presentations, or Bloomberg.

Endnote: Unless otherwise noted, all company-specific data derived from internal analysis, company presentations, Bloomberg, or independent sources. Values as of 3.31.21, unless otherwise noted.

This document is not an offer to sell or the solicitation of an offer to buy interests in any product and is being provided for informational purposes only and should not be relied upon as legal, tax or investment advice. An offering of interests will be made only by means of a confidential private offering memorandum and only to qualified investors in jurisdictions where permitted by law.

An investment is speculative and involves a high degree of risk. There is no secondary market for the investor’s interests and none is expected to develop and there may be restrictions on transferring interests. The Investment Advisor has total trading authority. Performance results are net of fees and expenses and reflect the reinvestment of dividends, interest and other earnings.

Prior performance is not necessarily indicative of future results. Any investment in a fund involves the risk of loss. Performance can be volatile and an investor could lose all or a substantial portion of his or her investment.

The information presented herein is current only as of the particular dates specified for such information, and is subject to change in future periods without notice.