By Kieran Brennan

•

January 18, 2025

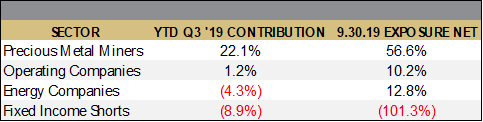

Dear Partners and Friends, PERFORMANCE Equinox Partners Precious Metals Fund, L.P. fell -12.9% in the fourth quarter, finishing the year down – 2.9%. The fund’s performance reflects the lackluster performance of the gold mining sector as well as the underperformance of the companies we own. While there were some clear themes, such as producing companies outperforming exploration companies, our 2024 results are most accurately captured through a description of our six best and six worst performing investments during the year. These twelve companies capture every investment that contributed at least 1%, positive or negative, to our 2024 fund performance. A Challenging Year In 2024, the gold price finished up +27.4%. The GDXJ ETF which tracks the index of junior gold mining producers was up +15.7%. Our portfolio of miners in this fund was down -2.9%. The underperformance of the gold miners as compared to gold largely reflects government participation in the gold market. In 2024, governments bought gold, not gold miners. The poor performance of the gold miners also reflects the sector’s continued subpar returns on capital. The S&P TSX Global Gold universe, a group of large, mature gold miners, only generated an 11% ROE in 2024 and a 5.4% free cash flow yield according to RBC. Despite their inadequate returns on capital, producing miners handily outperformed most exploration and development companies. There remains almost no market for most gold mining companies that are years away from first production. As value investors with contrarian instincts, we have found the increasingly irrational valuations of the pre-revenue companies of particular interest. Often as a project advances, the equity market value of the company declines. These share price declines in turn create a self-reinforcing dynamic in which the small, cash-starved companies underperform because they don’t have access to the capital necessary to move their projects forward. At this point, the downward spiral of pre-revenue gold miners is very extended and nearing a floor in our opinion. Not only are the valuations of these companies incredibly low, but these companies have become increasingly attractive acquisition targets. Although exploration companies are the most severely discounted sector, 54% of our fund remains invested in producing companies. In general, our producing companies trade at a discount to the sector because they are executing on significant capex plans and lack free cash flow. During construction periods, the market can become excessively skeptical. This skepticism, in turn, can present an opportunity to buy high quality assets run by good management teams at attractive valuations. We believe that this is clearly the case at Eldorado Gold, K92 Mining, West African Resources and Adriatic Metals. Overall, our miners are incredibly cheap. Assuming a flat gold price, we estimate our producers will generate a 23.5% IRR. Our companies that do not yet generate any cash flow are cheaper still. Ascot, Thesis, Troilus and Goldquest, for example, have an average IRR of over 30% at current metals prices. Six Winners and Six Losers in 2024 Note: Below IRR is our Equinox internally calculated IRR based on 2024 year-end market prices and forecasted future FCF per share to equity. Borealis Mining: 2024 Performance +29%, IRR 48% Borealis was founded by Kelly Malcolm in 2023 to leverage a large heap leach facility in Nevada by acquiring nearby low-grade heap leach assets. We invested in a pre-IPO round at a $30M post-money valuation. At the time, Borealis had approx. $5M worth of crushed stockpiles, a fully permitted heap leach facility, ~60,000oz of reserves ready to be processed with limited capex and substantial exploration potential at depth. In late 2024, Borealis began to acquire nearby deposits. Borealis purchased Bull Run for $6M in cash. This translates to $14 per ounce for ~500,000oz of already defined resources, and confirms managements intuition that there are small, stranded assets for sale in Nevada. We expect Borealis to continue this acquisition strategy and ramp to become a ~75,000 oz per year producer. K92 Mining: 2024 Performance +22%, IRR 17% K92 controls the world-class Kainantu mine in the highlands of Papua New Guinea. This mine is a high-grade, low-cost asset with a 3 million oz resource at 7g/t. K92 produced 120,000 oz last year, and we expect the company’s Phase 3 expansion will take annual production to over 150,000 oz (gold equivalent) in 2025. While K92 has often struggled to meet its ambitious growth targets, the company has strung together two consecutive quarters of meaningfully higher production with higher than reserve grades. K92 recently expanded the milling capacity which had been a meaningful bottleneck for years. If the company can reach Phase 4, the Kainantu mine’s production will produce ~400,000 oz at a bottom quartile cash cost of <$1000/oz while maintaining a clean balance sheet with minimal leverage. West African Resources: 2024 Performance +38%, IRR 31% In 2024, West African Resources (WAF) remained on-time and on budget in the build of the company’s second mine in Burkina Faso, called Kiaka. Once Kiaka is commissioned in Q3 2025, WAF will be a ~450,000 oz annual producer for the next 10 years. While the construction has proceeded as expected, WAF was adversely impacted by the local content language in Burkina Faso’s new mining code. Rather than pay the resulting mark up in their rental of local equipment, WAF elected to purchase their mining fleet outright. This decision added $150 million to the company’s capital budget and resulted in a July equity raise of the same amount. While we were disappointed with the need for more equity capital, ultimately the raise will accelerate WAF’s buy-back and dividend plans. If the company continues to trade at the current valuation, we expect the board will announce a sizable share repurchase as soon as the company’s debt is repaid. Hochschild Mining: 2024 Performance +96%, IRR 18% Hochschild Mining (HOC) is a proven mine builder with the strategy of reinvesting free cash flow into new projects to grow production. In 2024, we visited their newly commissioned mine in Brazil, called Mara Rosa, which was successfully built on time and on budget. Mara Rosa will deliver a 20%+ project level IRR and highlights HOC's competence in executing medium-size projects in Latin America. We expect the company will be able to repeat this success with another mine in Brazil, the Monte Do Carmo project in the neighboring state of Tocantins. Big picture, HOC is a family-owned business with a goal of producing 500,000 ounces of gold per year by 2030. While we would prefer a return on capital goal rather than a growth target, we appreciate the straight-forward way the company organizes its operations, and we believe the company will not undertake projects with less than a 20% cash on cash IRR. Moreover, unlike many growth miners, when the company reaches their targeted 500,000 ounces of annual production – anticipated for 2030 - we expect HOC to transition to return free cash flow to shareholders. Galiano Gold: 2024 Performance +35%, IRR 29% Galiano has been busily working on a new mine plan which will be released on January 28th. We expect the company’s production guidance will increase as Galiano elects to move forward with the redevelopment of their higher grade Nkran pit. We also expect increased exploration spending in 2025 as the company ramps up work on their newly consolidated land package. We are expecting Galiano to guide to a production target of approx. 250,000 ounces per year by 2027. Even at this higher rate of production, we anticipate the company will be able to more than replace reserves given the prospectivity of the Asankrangwa gold belt in which they operate. While Galiano will have to reinvest the vast majority of its cash flow in growth in 2025 and 2026, the company should become a substantial free cash flow generator beginning in 2027. Solidcore Resources: 2024 Performance +22%, IRR 21% Solidcore, a spin-out from Polymetal, is a new position in our fund. Solidcore is run by CEO Vitaly Nesis, and controlled by Oman’s sovereign wealth fund. The company operates two long-lived mines in Kazakhstan and produces 480,000 ounces of gold annually at a competitive All-In Sustaining Cost (AISC) of $1,300/oz. With an EV/EBITDA multiple of 2.2x, Solidcore trades at an almost 50% discount to its peers. This undervaluation is largely due to the company’s sole listing on the Astana International Exchange in Kazakhstan. We expect Solidcore to generate roughly $400 million in free cash flow per year at current gold prices. In 2025 and 2026, this free cash flow will be invested in a new pressure oxidation autoclave. Beginning in 2027, we anticipate that $100 million USD of the company’s free cash flow will be distributed to shareholders. This prospective dividend along with the company’s plan to re-list on the London Stock Exchange offers two catalysts that should drive a significant re-rating. Orezone Gold: 2024 Performance -30%, IRR 27% While Orezone completed its initial build on time and on budget, the company failed to generate the free cash flow necessary to internally finance the expansion of its operations in Burkina Faso. The company’s reliance on high-cost diesel generators and an unreliable power grid proved particularly problematic. Largely due to higher-than-expected power costs, the midpoint of their AISC guidance increased by $100/oz from last year’s projection of $1,338/oz. Despite the elevated power costs, Orezone successfully closed their financing for the hard rock processing plant in December 2024. This financing will enable Orezone to increase annual production from approx. 120,000 oz in 2024 to ~180,000 oz in 2026. We expect 2025 to be a pivotal year for the company as they will begin to generate sufficient cash to pay down debt and continue building towards their 250,000 oz/year target. We are also encouraged by the company’s ongoing exploration program which has the potential to increase the Bombore’s mine life at higher grades. C3 Metals: 2024 Performance -62% C3 stock declined significantly in 2024 even as the company made significant progress advancing their projects in both Jamaica and Peru. With respect to their Jamaican asset, C3 Metals signed a joint venture agreement with the Stewart family, one of the wealthiest families on the island. C3 is now well-positioned to do a JV deal with a larger international mining company that can finance the costly deep holes necessary to test the porphyry copper deposit’s potential. In Peru, C3 Metals received a permit to access one of its land packages located just 40 kilometers east of MMG’s Las Bambas mine. This permit, which took years to secure, opens the door for further exploration in a proven copper-rich region. With the permit in hand, C3 Metals should be able to bring in a larger partner to drill out the asset. Troilus Gold: 2024 Performance -45%, IRR 35% In May 2024, Troilus submitted its feasibility study to the Canadian government. This new study detailed their plan to develop a 22-year open pit mine that would produce approx. 300,000 oz of gold per year. With current gold prices north of $2,600 and copper hovering around $4, the project will likely move forward. The company has received financial support from a handful of export credit agencies interested in its 10% copper production. Troilus is also in the final stages of submitting the Environmental and Social Impact Assessment (“ESIA”), another key milestone as they advance towards construction. Located 300 kilometers north of Chibougamau, Quebec, the Troilus project is a brownfield site in a favorable mining jurisdiction with the potential to become a Top 10 copper gold project in Canada. We are fans of CEO Justin Reid and believe in his ability to permit the project and advance it towards becoming a premier North American copper-gold producer. At a $4/oz equity market cap to gold equivalent ounces in ground ratio, we believe Troilus is one of Canada’s best leveraged investments to rising gold and copper prices. Ascot Resources: 2024 Performance -23%, IRR 38% Ascot Resources put its Premier gold project on care & maintenance in September of 2024. At the time, the company didn’t have enough ore coming from the underground mine to profitably operate the 2,500 tonnes per day mill. To rectify the lack of available ore, the company raised $43 million, extended the term of their debt, and decided to invest in an additional 2,500 meters of development before commissioning the mill. The board then made a change at CEO and brought in Jim Currie for his extensive underground mining experience and added our own Coille Van Alphen to the board. Underground development is currently underway, and we expect the mill to restart in Q2 2025. One more injection of capital will likely be required to ensure the company has a sufficient working capital buffer as they restart the mill. When the mine reaches commercial production, it will be able to generate a sustainable ~$100m of FCF per year which should translate into a stock price of at least $1 CAD per share. Great Pacific Gold: 2024 Performance -47% Great Pacific owns two highly prospective gold exploration projects in Papua New Guinea (PNG). Over the course of 2024, the company refined its exploration targets and drilled 5000m at its Kesar project in the highlands of PNG. The Kesar project looks to be an extension of nearby K92’s mine, and as such may be sold to K92. Great Pacific will begin drilling exploration targets at its second PNG property in Q2 of 2025. This property is a brownfield site with past production at a grade of more than 10 g/t. Great Pacific has a third asset in Australia, which we believe could be sold to fund the company’s exploration activities in PNG. Great Pacific is led by an excellent CEO in Greg McCunn. We got to know Greg through a previous investment in West Africa. As CEO, he brings the necessary vision, discipline, and accountability to an exploration company. We believe the company will deliver exploration success at their two PNG assets and ultimately enable Greg to create shareholder value in a variety of ways. GoGold Resources: 2024 Performance -24%, IRR 30% GoGold has been waiting two years for its permit in Mexico. The delay was caused by the previous Mexican President Andres Manual Lopez Obrador’s (AMLO) staunch opposition to new mining development. In the end, while neither of AMLO’s major proposed changes to the mining code passed, few mining permits of any kind were issued during his time in office. GoGold’s large cash buffer and existing heap leach operation enabled the company to wait out AMLO without needing to raise additional equity capital. We think their patience will soon be rewarded as the new administration of President Claudia Sheinbaum plans to process permit applications on their technical merits. In GoGold’s case, the technical merits of their Los Ricos South project are exceptionally strong with over 100 million oz of silver at an average grade of 276 g/t. Sincerely, Equinox Partners Investment Management